Table of Content

- How much income do you need to get a reverse mortgage?

- For reverse mortgage loans with case numbers assigned on or after August 4, 2014

- How We Make Money

- Cash Reserve for Seniors: The Special Benefits of a Reverse Mortgage ‘Line of Credit’

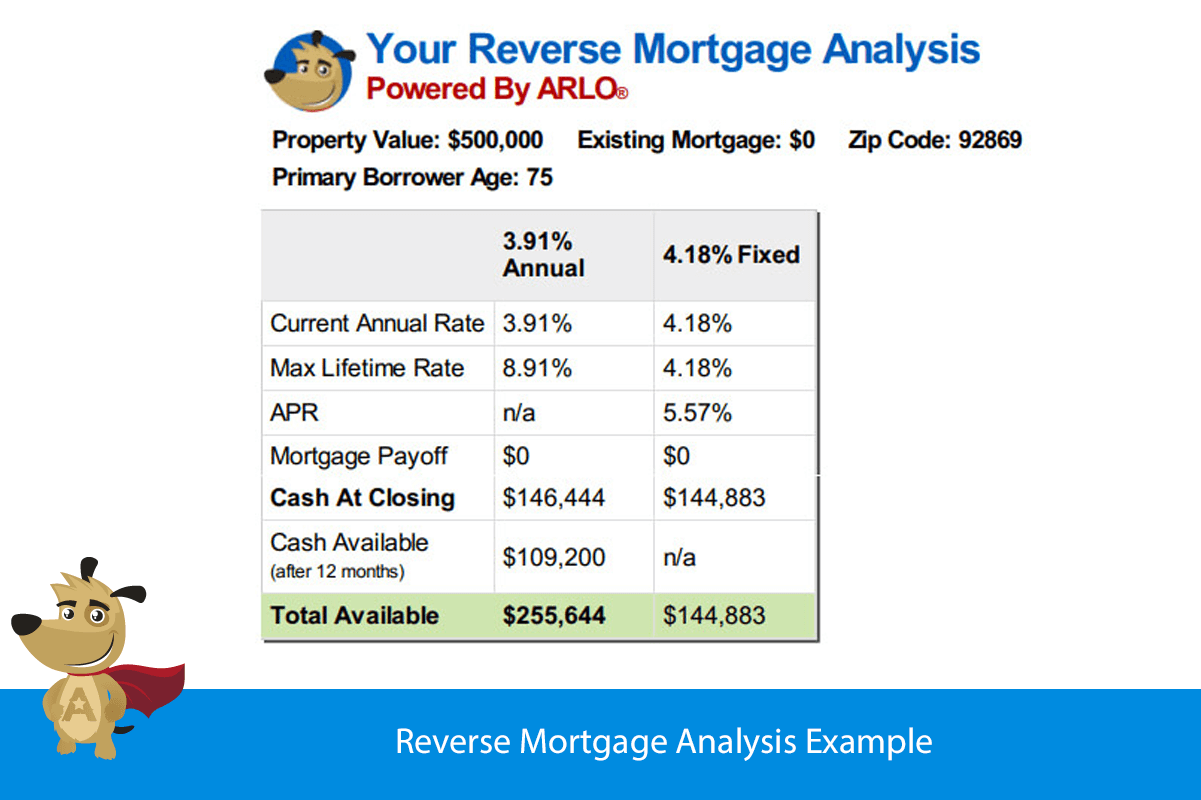

- America’s #1 rated reverse mortgage lender

- Benefits and Drawbacks of a Reverse Mortgage

If you buy these products, you could lose the money you get from your reverse mortgage. You don’t have to buy any financial products, services, or investment to get a reverse mortgage. In fact, in some situations, it’s illegal to insist that you buy other products to get a reverse mortgage. A reverse mortgage lets you borrow money based on the equity you have in your home — but it’s not the same as a home equity loan or a home equity line of credit . For an eligible non-borrowing spouse, deferral means the lender doesn’t say, “Hey, your loan is due.

A reserve mortgage is still a good option for some, even with these risks. If you're considering one, I recommend starting with HUD counseling; here's a list of approved agencies. The grocery bag represents $357.40, which according to the USDA is the monthly grocery bill for an extremely thrifty elderly couple. The car represents the average car insurance of about $150 per month; the light bulb is the average electricity bill of $103.67; and the smartphone represents the average cellphone bill of $111. After adding up those costs, there's about $30 left for a night out at a decent restaurant. The non-borrowing spouse is also protected if the borrower becomes incapacitated.

How much income do you need to get a reverse mortgage?

Still, in terms of keeping the reverse mortgage program financially viable while also allowing senior homeowners to get reverse mortgages with some non-borrowing spouse protections, the U.S. Department of Housing and Urban Development believes that the rules do make sense. A Reverse Mortgage is a loan product secured by a principle residence enabling the homeowner to access the equity of the home and not make traditional mortgage payments on the loan. According to a recent study, 93% of Canadians want to remain in their home as they age. Access to traditional lending becomes limited for seniors as the income isn’t always there to support the lender guidelines.

Also, a HECM borrower generally can live in a nursing home or other medical facility for up to 12 consecutive months before they have to repay the loan. Stop and check with a counselor or someone you trust before you sign anything. A reverse mortgage can be complicated and isn’t something to rush into. A maturity event is when something happens that triggers the repayment of a reverse mortgage. A home equity conversion mortgage is a type of Federal Housing Administration insured reverse mortgage. This nonprofit looks to reform reverse mortgages in the U.S. by reducing foreclosures and making the Mutual Mortgage Insurance Fund more sustainable.

For reverse mortgage loans with case numbers assigned on or after August 4, 2014

Losing your reverse mortgage proceeds may require you to sell your home if the loan was not structured properly based on your retirement needs. Or, you can choose to receive monthly payments for a set period of time and then switch to a line of credit when you no longer need the income. For example, you could choose to receive a lump sum of cash to pay off your mortgage and then opt for a line of credit to have access to money in the future if you need it.

The key is to make sure you are current on the items that you must continue to pay during the terms of the reverse mortgage. That includes paying your property taxes, your home insurance and any necessary home repairs. If you fall behind, or fail to pay, any of these items, your lender has the option to accelerating your reverse mortgage and making the whole sum due, which could leave you at risk of foreclosure. One way to avoid this issue is to maintain an escrow account for these expenses. Even after learning about inverted mortgages and considering the pros and cons and carefully choosing to get the loan to achieve your goals, you may want to get out of your reverse mortgage. No matter how few dollars you get through a reverse mortgage, it ensures that you can live in your house forever.

How We Make Money

We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. If your loan requires you to carry flood insurance, you must also keep up with those premiums. This is a great question – is it better to get a mortgage from a bank or mortgage company. There are benefits and short comings with any mortgage product, be it from a mortgage company, or from a bank.

Part 79 applies to both proprietary and HECM reverse mortgage loans. A reverse mortgage might sound a lot like a home equity loan or line of credit. Indeed, similar to one of these loans, a reverse mortgage can provide a lump sum or a line of credit that you can access as needed based on how much of your home youve paid off and your homes market value. But unlike a home equity loan or line of credit, you dont need to have an income or good credit to qualify, and you wont make any loan payments while you occupy the home as your primary residence. A reverse mortgage allows homeowners who are 62 or older to access their home equity without selling the house or taking on extra monthly payments.

The borrower or their heirs are also protected if the lender goes out of business. With a line of credit, you have an approved amount of money that you can borrow against when you need it. This can be a good option if you want to supplement your income or if you need a set amount of money each month to cover your living or long-term care expenses . It’s important to keep up with the maintenance of your home when you have a reverse mortgage.

If you own a home appraised at a high value , you may be able to get more money. It can be an expensive way to borrow money that limits your options down the road. About the potential risks, how reverse mortgages work, and how to get the best deal for you, and how to report reverse mortgage fraud. You’ve opened all your gifts, and now it’s time to open those post-holiday credit card statements. If you were a little too jolly with your holiday spending, here are some tips to help you pay down your credit card debt.

As you can imagine, this can help you out quite a lot financially. If you’re looking to buy a home that’s been on the market for more than a year, it’s a good idea to check with your lender first to make sure the property is still in good condition. If it isn’t, then you may want to consider selling it to someone else. Interest and fees accrue throughout the loan term while your home equity decreases. The loan becomes due when you sell the home, move out, fall behind on property charges, or die.

If you get a proprietary reverse mortgage, there are no set limits on how much you can borrow. There are risks to reverse mortgages, so you should do your research, contact a HUD-approved counselor and choose an FHA-approved HECM lender. Understanding the above property rules helps senior homeowners better position themselves to successfully apply for a reverse mortgage. Reverse mortgages are designed to help older homeowners access their home equity, providing a potentially much-needed source of income when they might be house rich, cash poor. If you dont qualify for any of these loans, what options remain for using home equity to fund your retirement? You could sell and downsize, or you could sell your home to your children or grandchildren to keep it in the family, perhaps even becoming their renter if you want to continue living in the home.

This means that the lender cannot cancel or reduce it due to changes in the economy, your finances, or the value of your home. You're not in danger of losing access to a reverse mortgage line of credit like you do with a HELOC. Many seniors are taking advantage of their home equity by applying for a reverse mortgage.

If this is the case, it may be necessary for you to file a petition with the court in order to get your property back. Fall behind on property charges, such as taxes, insurance, and HOA fees. Prepare any non-borrowing family members living in the home by deciding together what they will do after you die. Where this gets more complicated if you have to move into an assisted living facility or nursing home, or when you pass away. These terms vary and are addressed within each loan, so make sure you review all the details to determine what you are comfortable with before you sign. As long as the borrower does not ‘default’ under the agreement by breaching key obligations, the bank cannot force a sale of your home.

However, the only way to prove if interest is deductible is to keep a record that shows exactly how you used the funds from a reverse mortgage. But lenders have to evaluate your finances and make sure you can both pay back the loan and keep up the house when they’re deciding whether to approve and close your loan. The lender may require you to set aside the money to pay things like property taxes, homeowner’s insurance, and flood insurance. In a reverse mortgage, the money paid by the lender to the homeowner in reverse does NOT include the lender making property tax and hazard insurance payments on the property. Those payments must be made, and kept current, by the reverse mortgagor from his or her own resources. To be an eligible non-borrowing spouse, you must be married to the borrowing spouse from the time the reverse mortgage closes until the time the borrowing spouse dies or moves out.

Community Rules apply to all content you upload or otherwise submit to this site. She holds a Bachelor of Science in Finance degree from Bridgewater State University and helps develop content strategies for financial brands. We are Canada’s top rated mortgage brokers based in Burnaby, BC, Canada since 2000. Another factor is the location of the property the type of dwelling on the property and the overall marketability of the property. The location of the property must be in an urban centre, it cannot be a rural property or an agricultural zoned property. It must be the applicants’ owner occupied principle residence and this can either be a single family home, an apartment style condo, a high rise condo or a town home.

No comments:

Post a Comment